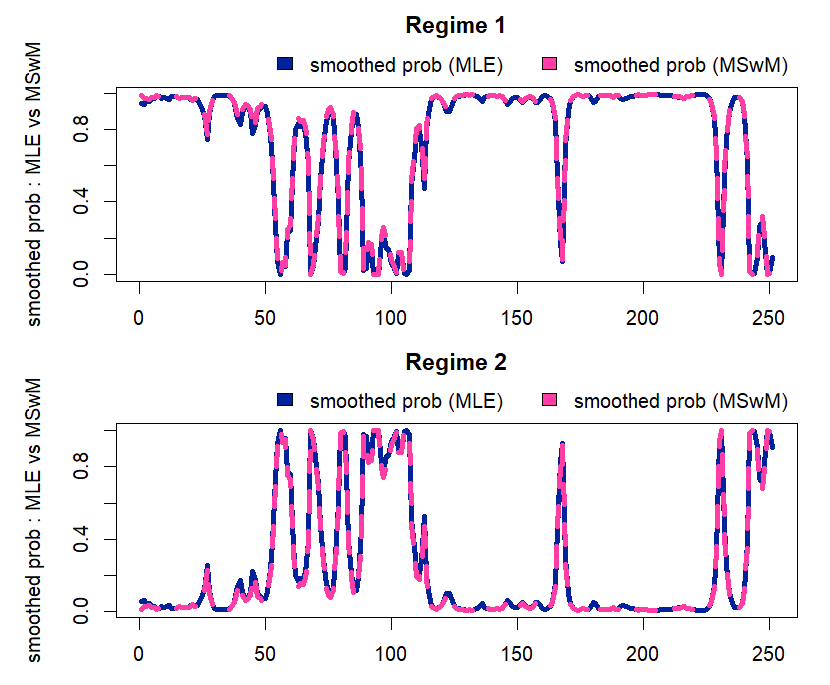

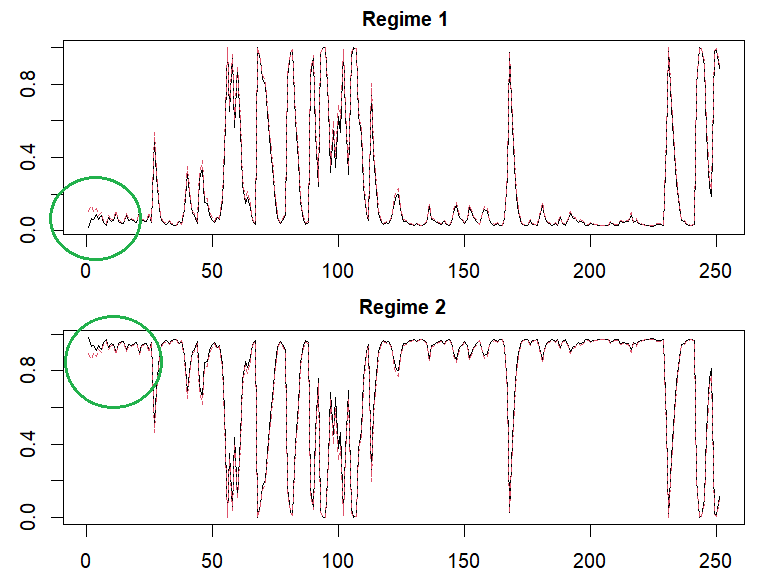

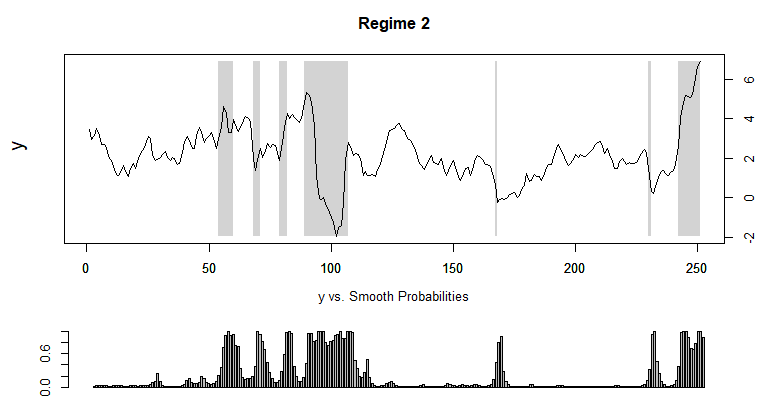

Kim (1994) Smoother Algorithm in Regime Switching Model using R code

This post explains smoothing algorithm of a regime switching model, which is known as Kim (1994) smoother. It is known that smoothing algorithm is more difficult to understand than filtering algorithm. For this perspective, I give detailed deriv...