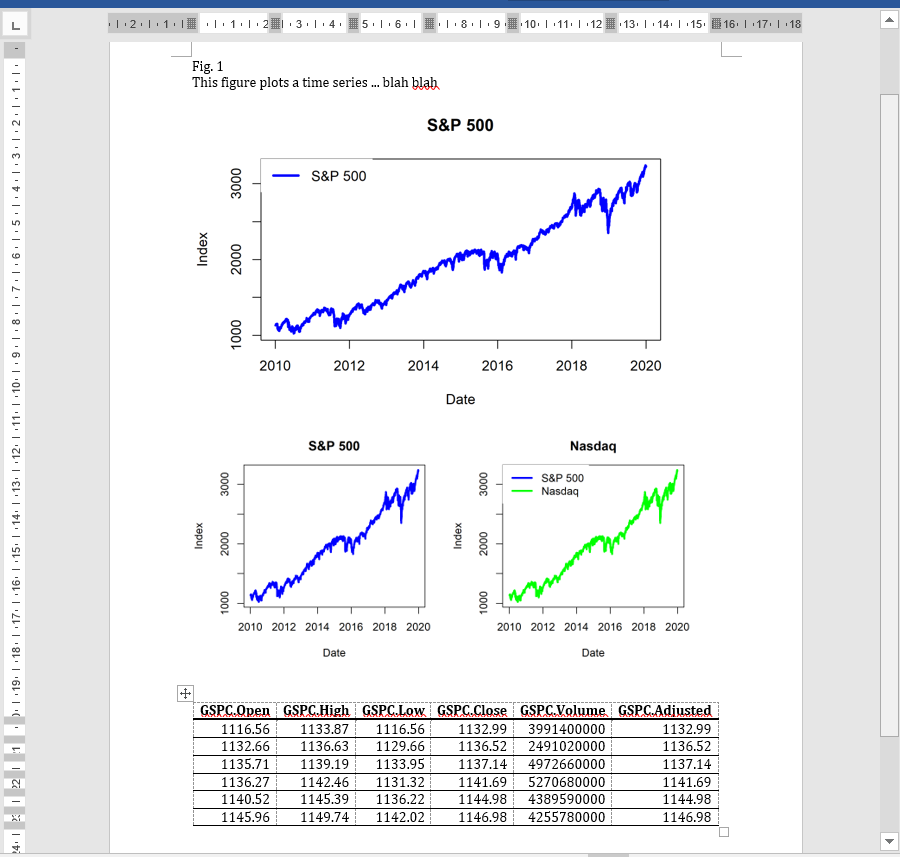

Paste R plot image into MS Word

This post explains how to paste R plot images into MS Word with some additional information such as title, description, and data table. This can be done by using the officer R package. Paste R plot image into MS Word with additional i...