Quality of Historical Stock Prices from Yahoo Finance

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

I recently looked at the strategy that invests in the components of S&P/TSX 60 index, and discovered that there are some abnormal jumps/drops in historical data that I could not explain. To help me spot these points and remove them, I created a helper function data.clean() function in data.r at github. Following is an example of how you can use data.clean() function:

##############################################################################

# Load Systematic Investor Toolbox (SIT)

# http://systematicinvestor.wordpress.com/systematic-investor-toolbox/

###############################################################################

setInternet2(TRUE)

con = gzcon(url('http://www.systematicportfolio.com/sit.gz', 'rb'))

source(con)

close(con)

###############################################################################

# S&P/TSX 60 Index as of Mar 31 2014

# http://ca.spindices.com/indices/equity/sp-tsx-60-index

###############################################################################

load.packages('quantmod')

tickers = spl('AEM,AGU,ARX,BMO,BNS,ABX,BCE,BB,BBD.B,BAM.A,CCO,CM,CNR,CNQ,COS,CP,CTC.A,CCT,CVE,GIB.A,CPG,ELD,ENB,ECA,ERF,FM,FTS,WN,GIL,G,HSE,IMO,K,L,MG,MFC,MRU,NA,PWT,POT,POW,RCI.B,RY,SAP,SJR.B,SC,SLW,SNC,SLF,SU,TLM,TCK.B,T,TRI,THI,TD,TA,TRP,VRX,YRI')

tickers = gsub('\\.', '-', tickers)

tickers.suffix = '.TO'

data <- new.env()

for(ticker in tickers)

data[[ticker]] = getSymbols(paste0(ticker, tickers.suffix), src = 'yahoo', from = '1980-01-01', auto.assign = F)

###############################################################################

# Plot Abnormal Series

###############################################################################

layout(matrix(1:4,2))

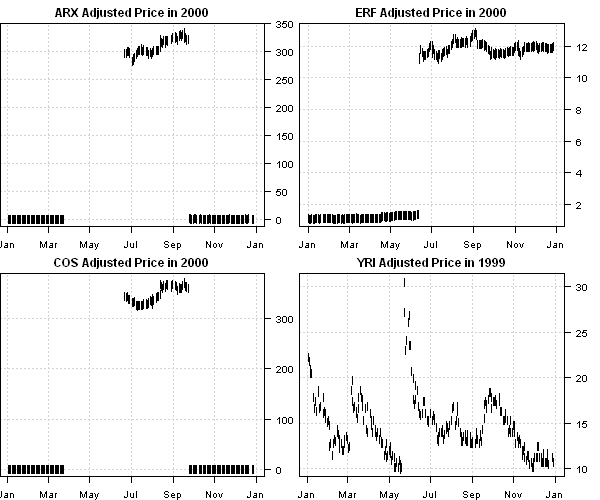

plota(data$ARX$Adjusted['2000'], type='p', pch='|', main='ARX Adjusted Price in 2000')

plota(data$COS$Adjusted['2000'], type='p', pch='|', main='COS Adjusted Price in 2000')

plota(data$ERF$Adjusted['2000'], type='p', pch='|', main='ERF Adjusted Price in 2000')

plota(data$YRI$Adjusted['1999'], type='p', pch='|', main='YRI Adjusted Price in 1999')

###############################################################################

# Clean data

###############################################################################

data.clean(data, min.ratio = 2)

> data.clean(data, min.ratio = 2) Removing BNS TRP have less than 756 observations Abnormal price found for ARX 23-Jun-2000 Ratio : 124.7 Abnormal price found for ARX 26-Sep-2000 Inverse Ratio : 99.4 Abnormal price found for COS 23-Jun-2000 Ratio : 124.1 Abnormal price found for COS 26-Sep-2000 Inverse Ratio : 101.1 Abnormal price found for ERF 14-Jun-2000 Ratio : 7.9 Abnormal price found for YRI 18-Feb-1998 Ratio : 2.1 Abnormal price found for YRI 25-May-1999 Ratio : 3

It is surprising that Bank of Nova Scotia (BNS.TO) has only one year worth of historical data. I also did not find an explanations for jumps in the ARX, COS, ERF during 2000.

Next, I did same analysis for the stocks in the S&P 100 index:

###############################################################################

# S&P 100 as of Mar 31 2014

# http://ca.spindices.com/indices/equity/sp-100

###############################################################################

tickers = spl('MMM,ABT,ABBV,ACN,ALL,MO,AMZN,AXP,AIG,AMGN,APC,APA,AAPL,T,BAC,BAX,BRK.B,BIIB,BA,BMY,COF,CAT,CVX,CSCO,C,KO,CL,CMCSA,COP,COST,CVS,DVN,DOW,DD,EBAY,EMC,EMR,EXC,XOM,FB,FDX,F,FCX,GD,GE,GM,GILD,GS,GOOG,HAL,HPQ,HD,HON,INTC,IBM,JNJ,JPM,LLY,LMT,LOW,MA,MCD,MDT,MRK,MET,MSFT,MDLZ,MON,MS,NOV,NKE,NSC,OXY,ORCL,PEP,PFE,PM,PG,QCOM,RTN,SLB,SPG,SO,SBUX,TGT,TXN,BK,TWX,FOXA,UNP,UPS,UTX,UNH,USB,VZ,V,WMT,WAG,DIS,WFC')

tickers.suffix = ''

data <- new.env()

for(ticker in tickers)

data[[ticker]] = getSymbols(paste0(ticker, tickers.suffix), src = 'yahoo', from = '1980-01-01', auto.assign = F)

###############################################################################

# Plot Abnormal Series

###############################################################################

layout(matrix(1:4,2))

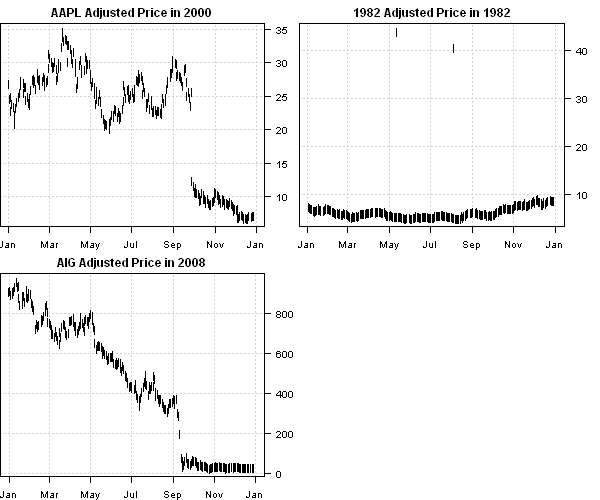

plota(data$AAPL$Adjusted['2000'], type='p', pch='|', main='AAPL Adjusted Price in 2000')

plota(data$AIG$Adjusted['2008'], type='p', pch='|', main='AIG Adjusted Price in 2008')

plota(data$FDX$Adjusted['1982'], type='p', pch='|', main='1982 Adjusted Price in 1982')

###############################################################################

# Clean data

###############################################################################

data.clean(data, min.ratio = 2)

> data.clean(data, min.ratio = 2) Removing ABBV FB have less than 756 observations Abnormal price found for AAPL 29-Sep-2000 Inverse Ratio : 2.1 Abnormal price found for AIG 15-Sep-2008 Inverse Ratio : 2.6 Abnormal price found for FDX 13-May-1982 Ratio : 8 Abnormal price found for FDX 06-Aug-1982 Ratio : 7.8 Abnormal price found for FDX 14-May-1982 Inverse Ratio : 8 Abnormal price found for FDX 09-Aug-1982 Inverse Ratio : 8

I first thought that September 29th, 2000 drop in AAPL was an data error; however, I found following news item: Apple bruises tech sector, September 29, 2000: 4:33 p.m. ET Computer maker’s warning weighs on hardware, chip stocks; Nasdaq tumbles.

So working with data requires a bit of data manipulation and a bit of detective works. Please, always have a look at the data before running any back-tests or making any conclusions.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.