Cointegration, Correlation, and Log Returns

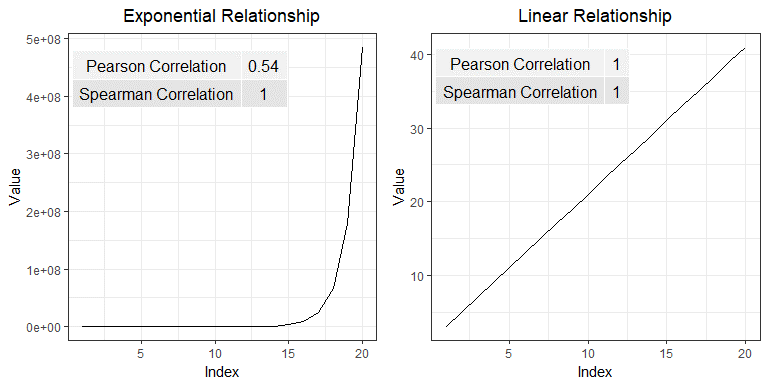

Co-Author: Eric Kammers I recently created a Twitter account for the blog where I will curate and comment on content I find interesting related to finance, data science, and data visualization. Please follow me at @Quantoisseur (see the embedded stream on the sidebar). Enjoy the post! The differences between correlation ...