Strategy 2: Riding the SMA Curve

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

This is the least complicated trend strategy in existance. You buy and hold the security as long as the security price is above a XXX-Day Simple Moving Average (SMA), and you can short it if it is below the SMA curve. The important question with this strategy is what the length in days of the SMA should be. We can run a test of different SMAs to see which one is most profitable/ least risky, and then choose accordingly. The intuition in choosing this should be based on an understanding of how long price trends usually last for a given security. This will obviously vary for different markets, different securities and across time periods.

A more technical approach to estimating the optimal variant of the SMA to use could be derived from one of the many parameter optimisation techniques avaiable through R, or through coding it yourself. These run the risk of curve-fitting, but as long as you are aware of the dangers associated with that, this could be one thing for you to try. I’ve found through experience that the 200-Day SMA works best for the S&P 500 as a whole, so I will be running this backtest using that.

Let’s say that if the market closes above its 200-Day Daily High SMA on any given day, we go long the next day and if it closes below it 200-Day Daily Low, we go short.

1-Get the data:

getSymbols(‘SPY’)

2-Calculate the 200-Day SMAs:

smaHi200=SMA(Hi(SPY),200)

smaLo200=SMA(Lo(SPY),200)

3-Calculate the lagged trading signal vector:

binVec=lag(ifelse(Cl(SPY)>smaHi200,1,0)+ifelse(Cl(SPY)

4-Get rid of the NAs:

binVec[is.na(binVec)]=0

5-Calculate returns vector and multiply out the trading vector with the returns vector to get the strategy return:

rets=diff(log(Ad(SPY)))

stratRets=binVec*rets

6-Run performance analytics:

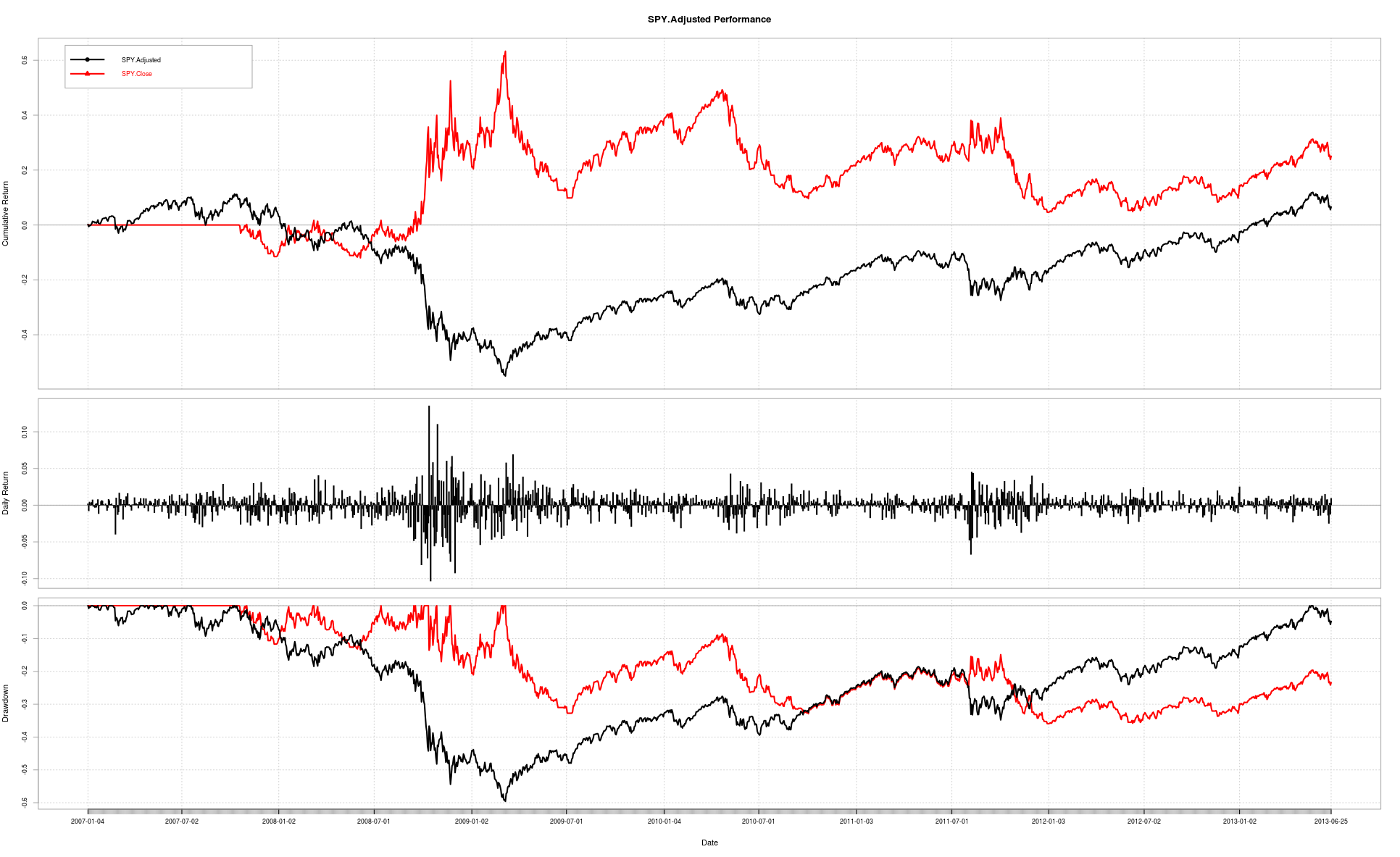

charts.PerformanceSummary(cbind(rets,stratRets))

Performance(stratRets)

Note: The Performance function I got from somewhere on the internet. I can’t remember where exactly so unfortunately I can’t directly credit the source. Regardless, I’m thankful to whoever wrote it. Here is the code:

Performance <- function(x) {

cumRetx = Return.cumulative(x)

annRetx = Return.annualized(x, scale=252)

sharpex = SharpeRatio.annualized(x, scale=252)

winpctx = length(x[x > 0])/length(x[x != 0])

annSDx = sd.annualized(x, scale=252)

DDs <- findDrawdowns(x)

maxDDx = min(DDs$return)

maxLx = max(DDs$length)

Perf = c(cumRetx, annRetx, sharpex, winpctx, annSDx, maxDDx, maxLx)

names(Perf) = c("Cumulative Return", "Annual Return","Annualized Sharpe Ratio",

"Win %", "Annualized Volatility", "Maximum Drawdown", "Max Length Drawdown")

return(Perf)

}

We get the following results (our sample period is 2007-01-01 to 2013-06-19):

Market

Cumulative Return: 0.10875991 Annual Return: 0.01613934

Annualized Sharpe Ratio: 0.06700363 Win %: 0.55157505

Annualized Volatility: 0.24087258 Maximum Drawdown: -0.59577736

Max Length Drawdown: 1411.00000000

Strategy

Cumulative Return: 0.30075987 Annual Return: 0.04159395

Annualized Sharpe Ratio: 0.17975121 Win %: 0.53215078

Annualized Volatility: 0.23139732 Maximum Drawdown: -0.35921405

Max Length Drawdown: 1078.00000000

So this strategy performed remarkably well compared to the market. 1-0 for Trend strategies! Looking at the graphs it’s easy to see the points where the strategy mirrors the market returns (and hence is short) and where the strategy follows the market returns (and hence is long). So does that mean we can start trading using this algorithm and make money? Not really- one important point to keep in mind is that backtesting can only be used to reject strategies, not to accept them. It is possible that this strategy can make money going forward, but who really know what the market will do? At least we can’t outright reject this strategy as useless.

What we are essentially saying is that under the conditions we used, our strategy was profitable. If those conditions were to continue, or repeat themselves, than we would have a profitable strategy in our hands. Are those conditions likely to repeat themselves? If market reactions to different stimuli are consistent across time, and if those stimuli re-occur then yes, perhaps. There’s also something to be said here about interactions between the different reactions or stimuli and on their subsequent effects on market outcomes. Is this something we can test for? Maybe, but its not something I’ll be getting into for now.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.