Quantitative Finance Applications in R – 6: Constructing a Term Structure of Interest Rates Using R (Part 1)

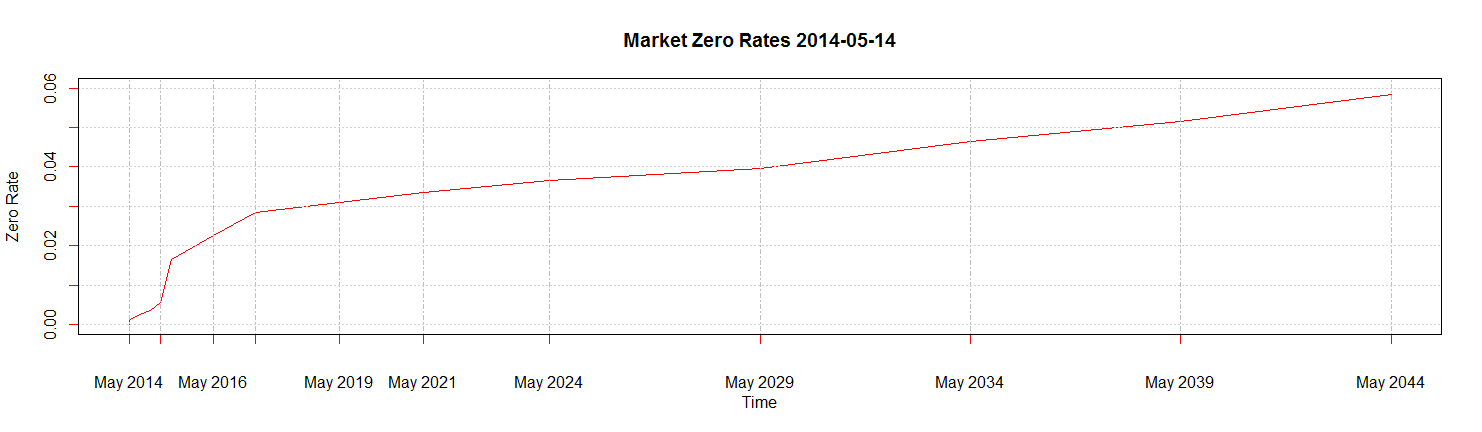

by Daniel Hanson Introduction Last time, we used the discretization of a Brownian Motion process with a Monte Carlo method to simulate the returns of a single security, with the (rather strong) assumption of a fixed drift term and fixed volatility. We will return to this topic in a future ...