KDA–Robustness Results

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

This post will display some robustness results for KDA asset allocation.

Ultimately, the two canary instruments fare much better using the original filter weights in Defensive Asset Allocation than in other variants of the weights for the filter. While this isn’t as worrying (the filter most likely was created that way and paired with those instruments by design), what *is* somewhat more irritating is that the strategy is dependent upon the end-of-month phenomenon, meaning this strategy cannot be simply tranched throughout an entire trading month.

So first off, let’s review the code from last time:

# KDA asset allocation

# KDA stands for Kipnis Defensive Adaptive (Asset Allocation).

# compute strategy statistics

stratStats <- function(rets) {

stats <- rbind(table.AnnualizedReturns(rets), maxDrawdown(rets))

stats[5,] <- stats[1,]/stats[4,]

stats[6,] <- stats[1,]/UlcerIndex(rets)

rownames(stats)[4] <- "Worst Drawdown"

rownames(stats)[5] <- "Calmar Ratio"

rownames(stats)[6] <- "Ulcer Performance Index"

return(stats)

}

# required libraries

require(quantmod)

require(PerformanceAnalytics)

require(tseries)

# symbols

symbols <- c("SPY", "VGK", "EWJ", "EEM", "VNQ", "RWX", "IEF", "TLT", "DBC", "GLD", "VWO", "BND")

# get data

rets <- list()

for(i in 1:length(symbols)) {

returns <- Return.calculate(Ad(get(getSymbols(symbols[i], from = '1990-01-01'))))

colnames(returns) <- symbols[i]

rets[[i]] <- returns

}

rets <- na.omit(do.call(cbind, rets))

# algorithm

KDA <- function(rets, offset = 0, leverageFactor = 1.5, momWeights = c(12, 4, 2, 1)) {

# get monthly endpoints, allow for offsetting ala AllocateSmartly/Newfound Research

ep <- endpoints(rets) + offset

ep[ep < 1] <- 1

ep[ep > nrow(rets)] <- nrow(rets)

ep <- unique(ep)

epDiff <- diff(ep)

if(last(epDiff)==1) { # if the last period only has one observation, remove it

ep <- ep[-length(ep)]

}

# initialize vector holding zeroes for assets

emptyVec <- data.frame(t(rep(0, 10)))

colnames(emptyVec) <- symbols[1:10]

allWts <- list()

# we will use the 13612F filter

for(i in 1:(length(ep)-12)) {

# 12 assets for returns -- 2 of which are our crash protection assets

retSubset <- rets[c((ep[i]+1):ep[(i+12)]),]

epSub <- ep[i:(i+12)]

sixMonths <- rets[(epSub[7]+1):epSub[13],]

threeMonths <- rets[(epSub[10]+1):epSub[13],]

oneMonth <- rets[(epSub[12]+1):epSub[13],]

# computer 13612 fast momentum

moms <- Return.cumulative(oneMonth) * momWeights[1] + Return.cumulative(threeMonths) * momWeights[2] +

Return.cumulative(sixMonths) * momWeights[3] + Return.cumulative(retSubset) * momWeights[4]

assetMoms <- moms[,1:10] # Adaptive Asset Allocation investable universe

cpMoms <- moms[,11:12] # VWO and BND from Defensive Asset Allocation

# find qualifying assets

highRankAssets <- rank(assetMoms) >= 6 # top 5 assets

posReturnAssets <- assetMoms > 0 # positive momentum assets

selectedAssets <- highRankAssets & posReturnAssets # intersection of the above

# perform mean-variance/quadratic optimization

investedAssets <- emptyVec

if(sum(selectedAssets)==0) {

investedAssets <- emptyVec

} else if(sum(selectedAssets)==1) {

investedAssets <- emptyVec + selectedAssets

} else {

idx <- which(selectedAssets)

# use 1-3-6-12 fast correlation average to match with momentum filter

cors <- (cor(oneMonth[,idx]) * momWeights[1] + cor(threeMonths[,idx]) * momWeights[2] +

cor(sixMonths[,idx]) * momWeights[3] + cor(retSubset[,idx]) * momWeights[4])/sum(momWeights)

vols <- StdDev(oneMonth[,idx]) # use last month of data for volatility computation from AAA

covs <- t(vols) %*% vols * cors

# do standard min vol optimization

minVolRets <- t(matrix(rep(1, sum(selectedAssets))))

minVolWt <- portfolio.optim(x=minVolRets, covmat = covs)$pw

names(minVolWt) <- colnames(covs)

investedAssets <- emptyVec

investedAssets[,selectedAssets] <- minVolWt

}

# crash protection -- between aggressive allocation and crash protection allocation

pctAggressive <- mean(cpMoms > 0)

investedAssets <- investedAssets * pctAggressive

pctCp <- 1-pctAggressive

# if IEF momentum is positive, invest all crash protection allocation into it

# otherwise stay in cash for crash allocation

if(assetMoms["IEF"] > 0) {

investedAssets["IEF"] <- investedAssets["IEF"] + pctCp

}

# leverage portfolio if desired in cases when both risk indicator assets have positive momentum

if(pctAggressive == 1) {

investedAssets = investedAssets * leverageFactor

}

# append to list of monthly allocations

wts <- xts(investedAssets, order.by=last(index(retSubset)))

allWts[[i]] <- wts

}

# put all weights together and compute cash allocation

allWts <- do.call(rbind, allWts)

allWts$CASH <- 1-rowSums(allWts)

# add cash returns to universe of investments

investedRets <- rets[,1:10]

investedRets$CASH <- 0

# compute portfolio returns

out <- Return.portfolio(R = investedRets, weights = allWts)

return(list(allWts, out))

}

So, the idea is that we take the basic Adaptive Asset Allocation algorithm, and wrap it in a canary universe from Defensive Asset Allocation (see previous post for links to both), which we use to control capital allocation, ranging from 0 to 1 (or beyond, in cases where leverage applies).

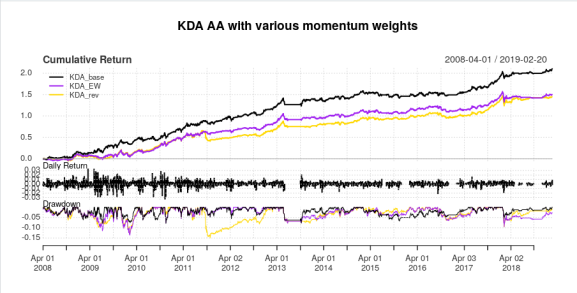

One of the ideas was to test out different permutations of the parameters belonging to the canary filter–a 1, 3, 6, 12 weighted filter focusing on the first month.

There are two interesting variants of this–equal weighting on the filter (both for momentum and the safety assets), and reversing the weights (that is, 1 * 1, 3 * 2, 6 * 4, 12 * 12). Here are the results of that experiment:

# different leverages

KDA_100 <- KDA(rets, leverageFactor = 1)

KDA_EW <- KDA(rets, leverageFactor = 1, momWeights = c(1,1,1,1))

KDA_rev <- KDA(rets, leverageFactor = 1, momWeights = c(1, 2, 4, 12))

# KDA_150 <- KDA(rets, leverageFactor = 1.5)

# KDA_200 <- KDA(rets, leverageFactor = 2)

# compare

compare <- na.omit(cbind(KDA_100[[2]], KDA_EW[[2]], KDA_rev[[2]]))

colnames(compare) <- c("KDA_base", "KDA_EW", "KDA_rev")

charts.PerformanceSummary(compare, colorset = c('black', 'purple', 'gold'),

main = "KDA AA with various momentum weights")

stratStats(compare)

apply.yearly(compare, Return.cumulative)

With the following results:

> stratStats(compare)

KDA_base KDA_EW KDA_rev

Annualized Return 0.10990000 0.0879000 0.0859000

Annualized Std Dev 0.09070000 0.0900000 0.0875000

Annualized Sharpe (Rf=0%) 1.21180000 0.9764000 0.9814000

Worst Drawdown 0.07920363 0.1360625 0.1500333

Calmar Ratio 1.38756275 0.6460266 0.5725396

Ulcer Performance Index 3.96188378 2.4331636 1.8267448

> apply.yearly(compare, Return.cumulative)

KDA_base KDA_EW KDA_rev

2008-12-31 0.15783690 0.101929228 0.08499664

2009-12-31 0.18169281 -0.004707164 0.02403531

2010-12-31 0.17797930 0.283216782 0.27889530

2011-12-30 0.17220203 0.161001680 0.03341651

2012-12-31 0.13030215 0.081280035 0.09736187

2013-12-31 0.12692163 0.120902015 0.09898799

2014-12-31 0.04028492 0.047381890 0.06883301

2015-12-31 -0.01621646 -0.005016891 0.01841095

2016-12-30 0.01253209 0.020960805 0.01580218

2017-12-29 0.15079063 0.148073455 0.18811112

2018-12-31 0.06583962 0.029804042 0.04375225

2019-02-20 0.01689700 0.003934044 0.00962020

So, one mea culpa: after comparing AllocateSmartly, my initial code (which I’ve since edited, most likely owing to getting some logic mixed up when I added functionality to lag the day of month to trade) had some sort of bug in it which gave a slightly better than expected 2015 return. Nevertheless, the results are very similar. What is interesting to note is that in the raging bull market that was essentially from 2010 onwards, the equal weight and reverse weight filters don’t perform too badly, though the reverse weight filter has a massive drawdown in 2011, but in terms of capitalizing in awful markets, the original filter as designed by Keller and TrendXplorer works best, both in terms of making money during the recession, and does better near the market bottom in 2009.

Now that that’s out of the way, the more interesting question is how does the strategy work when not trading at the end of the month? Long story short, the best time to trade it is in the last week of the month. Once the new month rolls around, hands off. If you’re talking about tranching this strategy, then you have about a week’s time to get your positions in, so I’m not sure the actual dollar volume this strategy can manage, as it’s dependent on the month-end effect (I know that one of my former managers–a brilliant man, by all accounts–said that this phenomena no longer existed, but I feel these empirical results refute that assertion in this particular instance). Here are these results:

lagCompare <- list()

for(i in 1:21) {

offRets <- KDA(rets, leverageFactor = 1, offset = i)

tmp <- offRets[[2]]

colnames(tmp) <- paste0("Lag", i)

lagCompare[[i]] <- tmp

}

lagCompare <- do.call(cbind, lagCompare)

lagCompare <- na.omit(cbind(KDA_100[[2]], lagCompare))

colnames(lagCompare)[1] <- "Base"

charts.PerformanceSummary(lagCompare, colorset=c("orange", rep("gray", 21)))

stratStats(lagCompare)

With the results:

> stratStats(lagCompare)

Base Lag1 Lag2 Lag3 Lag4 Lag5 Lag6 Lag7 Lag8

Annualized Return 0.11230000 0.0584000 0.0524000 0.0589000 0.0319000 0.0319000 0.0698000 0.0790000 0.0912000

Annualized Std Dev 0.09100000 0.0919000 0.0926000 0.0945000 0.0975000 0.0957000 0.0943000 0.0934000 0.0923000

Annualized Sharpe (Rf=0%) 1.23480000 0.6357000 0.5654000 0.6229000 0.3270000 0.3328000 0.7405000 0.8460000 0.9879000

Worst Drawdown 0.07920363 0.1055243 0.1269207 0.1292193 0.1303246 0.1546962 0.1290020 0.1495558 0.1227749

Calmar Ratio 1.41786439 0.5534272 0.4128561 0.4558141 0.2447734 0.2062107 0.5410771 0.5282311 0.7428230

Ulcer Performance Index 4.03566328 1.4648618 1.1219982 1.2100649 0.4984094 0.5012318 1.3445786 1.4418132 2.3277271

Lag9 Lag10 Lag11 Lag12 Lag13 Lag14 Lag15 Lag16 Lag17

Annualized Return 0.0854000 0.0863000 0.0785000 0.0732000 0.0690000 0.0862000 0.0999000 0.0967000 0.1006000

Annualized Std Dev 0.0906000 0.0906000 0.0900000 0.0913000 0.0906000 0.0909000 0.0923000 0.0947000 0.0949000

Annualized Sharpe (Rf=0%) 0.9426000 0.9524000 0.8722000 0.8023000 0.7617000 0.9492000 1.0825000 1.0209000 1.0600000

Worst Drawdown 0.1278059 0.1189949 0.1197596 0.1112761 0.1294588 0.1498408 0.1224511 0.1290538 0.1274083

Calmar Ratio 0.6682006 0.7252411 0.6554796 0.6578231 0.5329880 0.5752771 0.8158357 0.7493000 0.7895878

Ulcer Performance Index 2.3120919 2.6415855 2.4441605 1.9248615 1.8096134 2.2378207 2.8753265 2.9092448 3.0703542

Lag18 Lag19 Lag20 Lag21

Annualized Return 0.097100 0.0921000 0.1047000 0.1019000

Annualized Std Dev 0.092900 0.0903000 0.0958000 0.0921000

Annualized Sharpe (Rf=0%) 1.044900 1.0205000 1.0936000 1.1064000

Worst Drawdown 0.100604 0.1032067 0.1161583 0.1517104

Calmar Ratio 0.965170 0.8923835 0.9013561 0.6716747

Ulcer Performance Index 3.263040 2.7159601 3.0758230 3.0414002

Essentially, the trade at the very end of the month is the only one with a Calmar ratio above 1, though the Calmar ratio from lag15 to lag 21 is about .8 or higher, with a Sharpe ratio of 1 or higher. So, there’s definitely a window of when to trade, and when not to–namely, the lag 1 through 5 variations have the worst performances by no small margin. Therefore, I strongly suspect that the 1-3-6-12 filter was designed around the idea of the end-of-month effect, or at least, not stress-tested for different trading days within the month (and given that longer-dated data is only monthly, this is understandable).

Nevertheless, I hope this does answer some people’s questions from the quant finance universe. I know that Corey Hoffstein of Think Newfound (and wow that blog is good from the perspective of properties of trend-following) loves diversifying across every bit of the process, though in this case, I do think there’s something to be said about “diworsification”.

In any case, I do think there are some future research venues for further research here.

Thanks for reading.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.