Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

The banking sector has risen since the passing of the orthodox economic policies in Turkey. This article will analyze and model an exchange-traded fund tracking the Turkish banking index for projection for the upcoming year.

library(tidyverse)

library(timetk)

#TCMB(Central Bank of the Republic of Turkey) One-Week Repo Rate

df_tcmb_rates <-

read_csv("https://raw.githubusercontent.com/mesdi/blog/main/tcmb_funds.csv") %>%

janitor::clean_names() %>%

select(date = release_date, tcmb_rates = actual) %>%

mutate(date = case_when(str_detect(date," \\(.*\\)") ~ str_remove(date," \\(.*\\)"), #removing parentheses and the text within

TRUE ~ date) %>%

parse_date(date, format = "%b %d, %Y") %>%

floor_date("month") %m+% months(1),

tcmb_rates = str_remove(tcmb_rates, "%") %>% as.numeric()) %>%

#makes regular time series by filling the time gaps

pad_by_time(date, .by = "month") %>%

tidyr::fill(tcmb_rates, .direction = "up") %>%

drop_na()

#TAU-BIST Bank Index Equity (TRY) Fund (Equity Intensive Fund)

df_tau <-

read_csv("https://raw.githubusercontent.com/mesdi/blog/main/tau.csv") %>%

janitor::clean_names() %>%

mutate(date = parse_date(date, "%m/%d/%Y")) %>%

select(date, fund_price = price)

#Merging all the data frames

df_merged <-

df_tau %>%

left_join(df_tcmb_rates) %>%

drop_na()

#Anomaly analysis of the Fund Price

df_merged %>%

pivot_longer(cols = c(-date), names_to = "vars") %>%

filter(vars == "fund_price") %>%

anomalize(date, value) %>%

plot_anomalies(date)

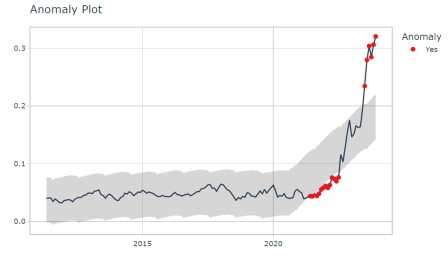

The anomaly plot of the fund prices confirms that shifting the policies has recently moved the fund values to a sharp upward trend.

We plan to use multiple algorithms to determine the best forecasting method. For this purpose, we will use the tidyAML package to compare all models. However, we will need to add the prophet model externally since it is not included in the package.

#Fast Regression witm many models

library(tidymodels)

library(modeltime)

library(tidyAML)

library(baguette)

library(bonsai)

#Split into a train and test set

splits <-

df_merged %>%

timetk::time_series_split(assess = "1 year", cumulative = TRUE)

train <- training(splits)

test <- testing(splits)

#Formula/preprocessing

df_rec <- recipe(fund_price ~ ., data = train)

#Modeling

df_reg <-

fast_regression(

.data = df_merged,

.rec_obj = df_rec,

.parsnip_fns = c("rand_forest",

"bag_tree",

"mars",

"bag_mars",

"boost_tree"

),

.parsnip_eng = c("ranger",

"earth",

"rpart",

"lightgbm")

)

#Adding the prophet Model

#Preprocessing/formula

rec_prophet <-

recipe(fund_price ~ ., data = train)

#Model specification

spec_prophet <-

prophet_reg() %>%

set_engine(engine = "prophet")

#Fitting workflow

set.seed(12345)

wflow_fit_prophet <-

workflow() %>%

add_recipe(rec_prophet) %>%

add_model(spec_prophet) %>%

fit(train)

#Augmented data

prophet_aug <-

broom::augment(wflow_fit_prophet, new_data = test) %>%

#Adding engine+function column

mutate(pfe = "prophet - prophet_reg")

#Plotting residuals distribution of all models

library(ragg)

df_reg %>%

mutate(res = map(fitted_wflw, \(x) broom::augment(x, new_data = test))) %>%

unnest(cols = res) %>%

mutate(pfe = paste0(.parsnip_engine, " - ", .parsnip_fns)) %>%

select(date,

fund_price,

tcmb_rates,

.pred,

pfe) %>%

rbind(prophet_aug) %>%

mutate(.res = fund_price - .pred) %>%

ggplot(aes(x = .res,

y = pfe,

fill = pfe)) +

geom_boxplot(show.legend = F) +

theme_minimal(base_family = "Bricolage Grotesque",

base_size = 16) +

labs(title = "Residuals by Fitted Model",

x = "",

y = "") +

theme(plot.title = element_text(hjust = 0.5))

Looking at the above chart, it seems reasonable to eliminate the prophet and lightgbm models from our workflow. We can then recalculate the accuracy of the remaining models and rank them accordingly.

#Modeling with rpart-bag_tree

#Model Specificaiton

mod_rpart <-

bag_tree() %>%

set_engine("rpart") %>%

set_mode("regression")

#Fitting

set.seed(12345)

wflw_fit_rpart <-

workflow() %>%

add_recipe(df_rec) %>%

add_model(mod_rpart) %>%

fit(train)

#Modeling with ranger-rand_forest

#Model Specificaiton

mod_ranger <-

rand_forest() %>%

set_engine("ranger") %>%

set_mode("regression")

#Fitting

set.seed(12345)

wflw_fit_ranger <-

workflow() %>%

add_recipe(df_rec) %>%

add_model(mod_ranger) %>%

fit(train)

#Modeling with earth - mars

#Model specification

mod_mars <-

mars() %>%

set_engine("earth") %>%

set_mode("regression")

#Fitting

set.seed(12345)

wflow_fit_mars <-

workflow() %>%

add_recipe(df_rec) %>%

add_model(mod_mars) %>%

fit(train)

#Modeling with earth-bagged_mars

#Model specification

mod_bagged_mars <-

bag_mars() %>%

set_engine("earth") %>%

set_mode("regression")

#Fitting

set.seed(12345)

wflow_fit_bagged_mars <-

workflow() %>%

add_recipe(df_rec) %>%

add_model(mod_bagged_mars) %>%

fit(train)

#Adding the fitted models to the model table

models_df <-

modeltime_table(wflw_fit_rpart,

wflw_fit_ranger,

wflow_fit_mars,

wflow_fit_bagged_mars) %>%

mutate(.function = c("bag_tree",

"rand_forest",

"mars",

"bag_mars"))

#Calibrating the models

cal_df <- modeltime_calibrate(models_df, new_data = test)

#Accuracy

cal_df %>%

modeltime_accuracy(metric_set = metric_set(rmse,rsq)) %>%

arrange(-rsq)

# A tibble: 4 × 6

.model_id .model_desc .function .type rmse rsq

<int> <chr> <chr> <chr> <dbl> <dbl>

1 3 EARTH mars Test 0.0445 0.885

2 1 RPART bag_tree Test 0.106 0.885

3 4 EARTH bag_mars Test 0.0510 0.848

4 2 RANGER rand_forest Test 0.125 0.675

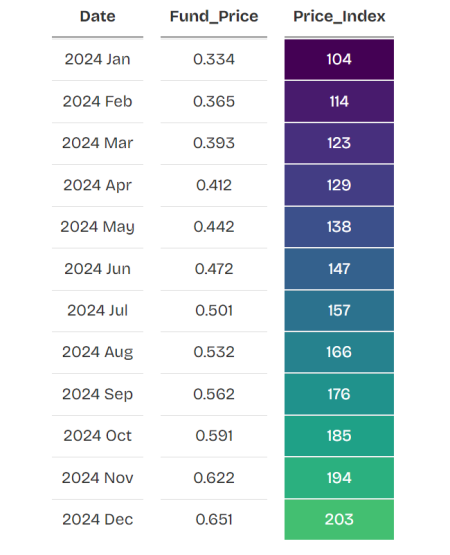

If we take rsq and rmse values into consideration, we’d better pick the mars model for forecasting. We will manually take next year’s tcmb_rates values that reflect predictions based on most economists in Turkey. We will create an additional variable (Price_Index) to see the percentage change from the last price.

#Forecasting

##Future(unseen) data frame

library(tsibble)

library(fable)

date <-

df_merged %>%

mutate(date = yearmonth(date)) %>%

as_tsibble() %>%

new_data(12) %>%

as_tibble() %>%

mutate(date = as.Date(date))

df_future <-

date %>%

mutate(tcmb_rates = c(rep(42.5,3),rep(45,9)))

#Re-fitting and forecasting

#Calibration data for mars

cal_mars <- modeltime_calibrate(wflow_fit_mars,

new_data = df_merged)

#Forecasted data frame

tau_fc <-

cal_mars %>%

modeltime_refit(df_merged) %>%

modeltime_forecast(new_data = df_future) %>%

select(Date = .index, Fund_Price = .value) %>%

mutate(Price_Index = (Fund_Price/ first(df_merged$fund_price)*100) %>%

round(0), #making 2023 Dec value = 100 to see the changes(%)

Fund_Price = round(Fund_Price, 3),

Date = yearmonth(Date))

#Making a forecasting table

library(kableExtra)

tau_fc %>%

kbl() %>%

kable_styling(full_width = F,

position = "center") %>%

column_spec(column = 3,

color= "white",

background = spec_color(tau_fc$Price_Index, end = 0.7)) %>%

row_spec(0:nrow(tau_fc), align = "c") %>%

kable_minimal(html_ = "Bricolage Grotesque")

It looks like that will double its value at the end of the coming year.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.