Announcing ESGtoolkit v0.1

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

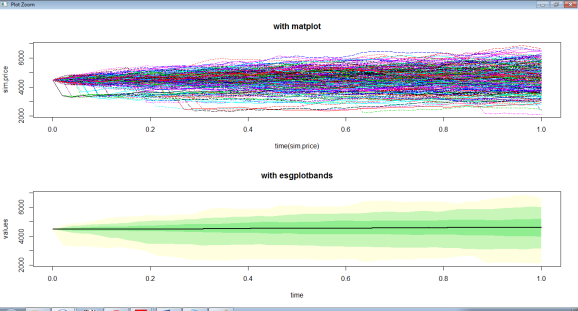

I’m pleased to announce the release on CRAN repositories, of our new R package : ESGtoolkit.

It’s a set of tools for Monte Carlo simulation of various models, involved in the construction of an Economic Scenario Generator (ESG), such as : equilibrium and no-arbitrage short rates models, equity models such as Black-Scholes, Merton, Heston and Bates (also known as Heston-Merton or Stochastic Volatility Jump diffusion), etc. The core loops of the simulations are made in C++.

In addition, a highly flexible correlation or dependence structure can be added between the simulations of different risk factors, with the use of vine copulas.

This note (the package’s vignette) will give you more insight on the features of this new package.

Comments and suggestions (constructive ? :)) are appreciated and highly valued.

.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.